The Federal Reserve’s Summary of Commentary on Current Economic Conditions—commonly referred to as the Beige Book—serves as the primary qualitative bridge between raw macroeconomic data and the localized operational realities of the twelve Federal Reserve Districts. While lagging indicators like the Consumer Price Index (CPI) provide a retrospective accounting of price changes, the Beige Book functions as a leading indicator of sentiment and pricing power. Current reporting across the districts signals a fundamental shift from demand-pull inflation toward a more complex, cost-push environment characterized by shrinking margins and asymmetric price sensitivity.

The Triad of Cost-Push Drivers

The recent acceleration in price pressures is not a monolithic event. It is the result of three distinct operational bottlenecks that have converged to force a re-evaluation of corporate pricing strategies. Meanwhile, you can find other events here: The Brutal Truth About the US Squeeze on Chinese Banks.

1. Labor Arbitrage Exhaustion

For the past decade, firms relied on a surplus of labor or globalized supply chains to suppress wage growth. That cycle has ended. In the current reporting cycle, districts highlight that while "headline" hiring has slowed, the cost of retaining specialized talent remains a non-negotiable expense. This creates a wage-price floor. Even as the labor market softens in aggregate, the specific skills required for high-output industries (advanced manufacturing, specialized healthcare, infrastructure) command premiums that firms must either absorb or pass through.

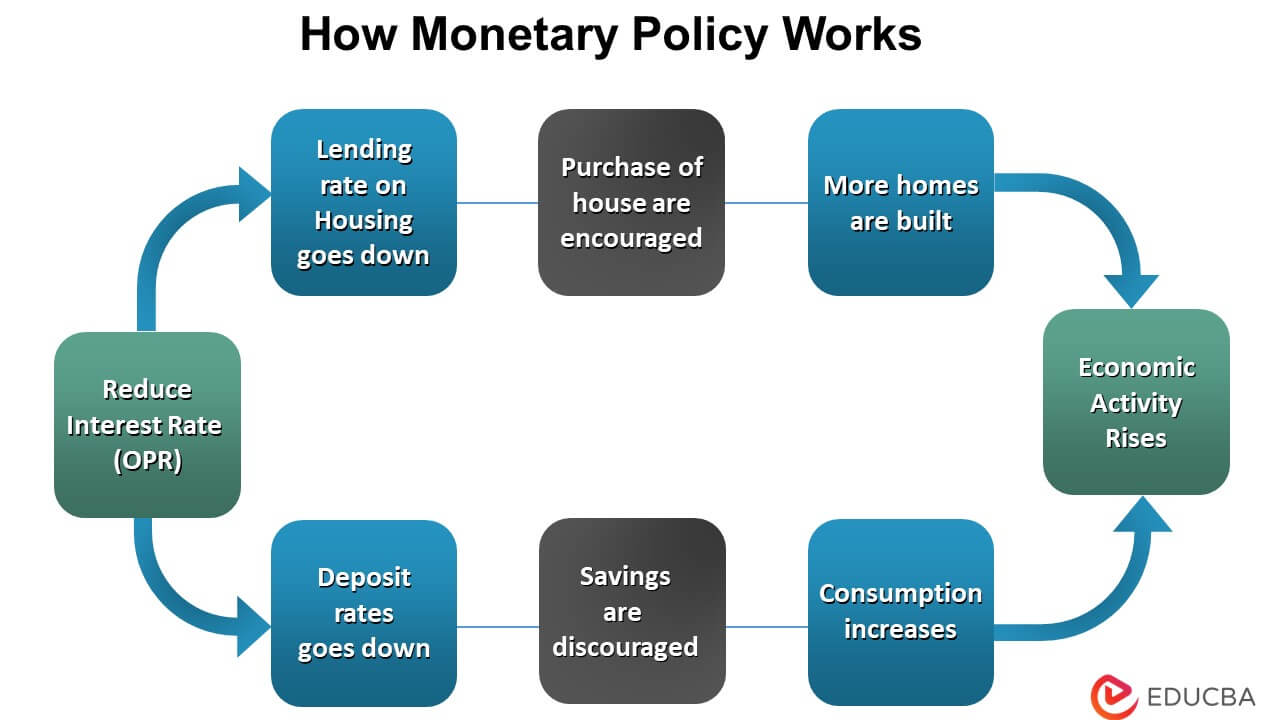

[Image of cost-push inflation diagram] To understand the complete picture, check out the detailed report by Bloomberg.

2. Supply Chain Friction and Input Volatility

Input costs are no longer tracking with standard commodity cycles. We see a decoupling where specific intermediate goods—particularly those tied to the energy transition or specialized electronics—experience localized hyper-inflation. The Beige Book data suggests that freight and logistics costs, which had stabilized post-2022, are once again trending upward due to geopolitical risk and infrastructure constraints. This creates a "staircase" cost function where expenses rise in sharp increments rather than a smooth curve.

3. The Regulatory and Insurance Tax

A frequently overlooked component in mainstream analysis is the surge in non-discretionary overhead. Reporting districts increasingly cite insurance premiums (property, casualty, and health) and regulatory compliance costs as primary drivers of price hikes. Unlike raw material costs, these expenses are "sticky"—they rarely revert to mean, creating a permanent increase in the break-even point for small and medium-sized enterprises (SMEs).

Price Elasticity and the Threshold of Resistance

The critical observation within the latest anecdotal evidence is the diverging ability of firms to maintain margins. We can categorize this into a two-tier pricing power framework.

Tier I: The Dominant Price-Makers

Companies with high brand equity or those providing essential utilities continue to pass through costs with minimal volume loss. In these sectors, the "pass-through rate" remains near 100%. The Beige Book suggests that these firms are not just covering costs but are utilizing the inflationary narrative to preemptively expand margins, a phenomenon often described as "excuse-based pricing."

Tier II: The Price-Takers and the Margin Squeeze

The majority of firms, particularly in retail and hospitality, are hitting the "elasticity ceiling." Consumers are responding to price increases with trade-downs—moving from premium brands to private labels or reducing the frequency of discretionary purchases.

The strategic limitation here is clear: When the rate of input cost growth exceeds the rate of consumer price acceptance, the result is margin compression rather than inflation. This is a deflationary signal for corporate earnings, even if it appears inflationary for the CPI.

The Transmission to Interest Rate Policy

The Federal Open Market Committee (FOMC) utilizes these qualitative reports to gauge whether inflation is becoming "entrenched." Entrenchment occurs when businesses and consumers stop viewing price hikes as transitory shocks and start incorporating them into long-term contracts and wage negotiations.

The current data shows that while price pressures are "increasing," they are doing so at a decelerating rate in certain sectors. This creates a divergence between "hard data" (which may stay high due to lagging shelter costs) and "soft data" (which shows a cooling in business intent).

The Velocity of Pricing Cycles

Historically, price adjustments occurred annually or semi-annually. The latest reports indicate a move toward "dynamic pricing" models, even in traditional B2B sectors. This increased velocity of price changes means that monetary policy, which operates with a "long and variable lag," risks being perpetually behind the curve. If the Fed waits for CPI to hit 2%, the Beige Book’s evidence of margin compression suggests they may have already over-tightened, triggering a credit contraction before the official data reflects it.

Sector-Specific Variance: A Granular Mapping

Manufacturing and Industrial Output

In the industrial heartland districts (Chicago, Cleveland), the focus has shifted from "getting parts" to "managing the cost of parts." Energy prices remain the primary variable. The shift toward electrification has created a dual-cost burden: firms are paying for traditional energy while simultaneously CAPEX-funding a transition to renewables. This "dual-stack" energy cost is a structural inflationary pressure that interest rate hikes are poorly equipped to solve.

Professional and Business Services

This sector reports the highest degree of wage pressure. The "quit rate" may be falling, but the "ask rate" for new hires remains elevated. We are observing a structural shortage of mid-level management and technical expertise, which acts as a bottleneck on productivity. If a firm cannot hire the person required to optimize a process, that process remains inefficient and expensive.

Real Estate and Construction

The paradox of high rates and high prices continues. While residential sales volume has cratered, the lack of inventory—driven by the "lock-in effect" of low-rate mortgages—keeps prices artificially high. Construction firms report that while lumber prices have moderated, the cost of skilled trades (plumbing, electrical) and land development remains at record highs.

The Operational Reality of "Higher for Longer"

The strategic implication of the current Beige Book findings is that the "Goldilocks" scenario—where inflation vanishes without a rise in unemployment—is increasingly unlikely. Firms are now forced to choose between three suboptimal paths:

- Direct Pass-Through: Risks a permanent loss of market share as consumers hit their debt limits.

- Product Shrinkflation/Skimpflation: Reducing quantity or quality to maintain price points. This is a short-term fix that erodes long-term brand equity.

- Efficiency Gains via Automation: High-margin firms are accelerating AI and automation deployments to offset labor costs. However, the high cost of capital (interest rates) makes this transition difficult for the Tier II firms that need it most.

Strategic Forecast for Q3 and Q4

Based on the synthesis of district reports, the economy is entering a "Phase of Attrition." The initial shock of inflation has passed, and we are now in the grind where balance sheets are tested.

The primary risk is a "margin cliff." As the savings cushion of the American consumer evaporates, the ability to absorb further price increases will vanish. Firms that have not optimized their cost structures over the last eighteen months will face a liquidity crunch.

Investors and analysts should shift their focus away from top-line revenue growth and toward EBITDA-to-Interest Expense ratios. In an environment of increasing price pressures and stagnant pricing power, the companies that survive are not the ones with the most sales, but the ones with the most resilient cost functions and the lowest dependency on rolling over short-term debt. Expect a surge in mid-market M&A as struggling firms are absorbed by those with the cash reserves to weather the margin squeeze. The tactical play is a flight to quality: prioritize entities with vertical integration that allows them to bypass the third-party cost-push pressures identified in the Fed’s latest reporting.